Curve Monthly Recap May–June 2026

May and June brought Llamalend V2 to Optimism, new activity across Curve markets from the YieldBasis V3 launch, a sweep to deprecate legacy Llamalend V1 markets, and rising veCRV fee flows, all while the crvUSD peg held firm through a broad market drawdown.

May and June delivered Curve's most significant lending release of the year, with Llamalend V2 launching on Optimism. Legacy V1 markets were deprecated across several chains, and crvUSD held its peg through a broad market drawdown.

This combined issue covers both months and includes a partner spotlight on YieldBasis V3 update, an independent protocol building on Curve infrastructure.

Key Highlights of May–June

- Llamalend V2 launched on Optimism, with the first three isolated markets activated through governance and a 100K OP incentive campaign that briefly pushed borrow rates below zero

- Lender protections expanded: a voluntary recovery pool for the CRV-long market, plus a veFunder gauge of up to 5M CRV for sDOLA-long2 borrowers

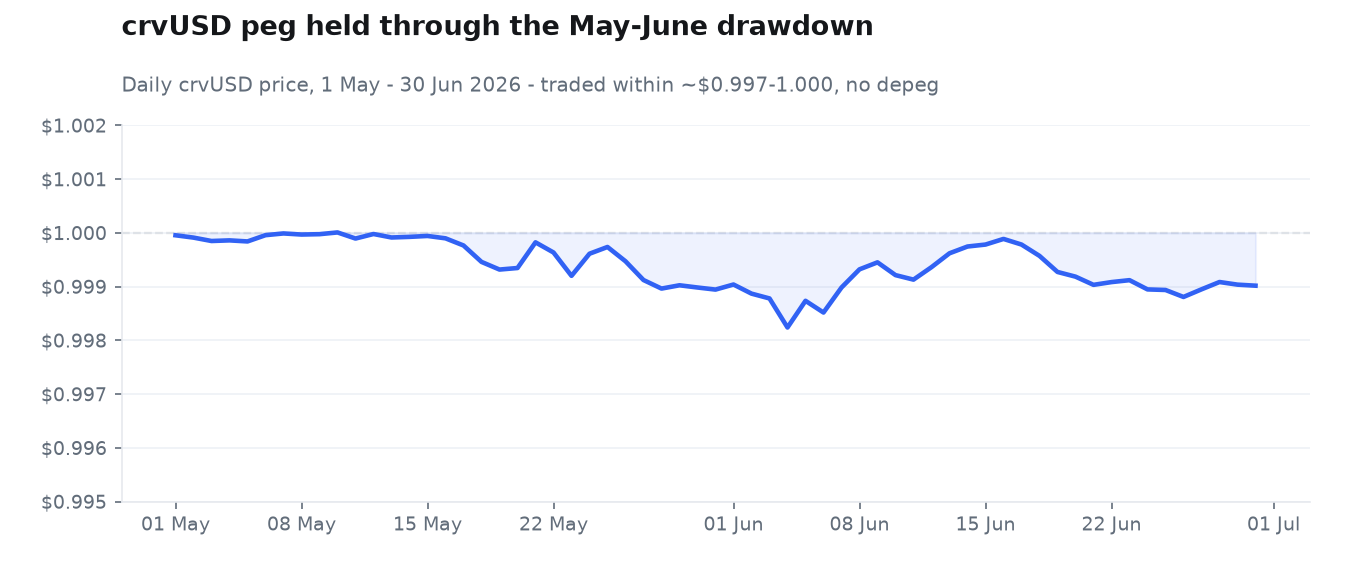

- crvUSD held its peg within ~$0.997–1.000 through the market decline, with no depeg episode at any point

- The share of crvUSD held in scrvUSD rose from ~36% to ~66%, deepening the peg's stability buffer

- veCRV APR climbed to ~5.4% as volatility-driven DEX fees peaked near $1.21M in a single week

- LlamaRisk concluded its Curve engagement on 30 June, returning its unvested crvUSD stream to the DAO treasury

- CRV bridging resumed on Sonic, Avalanche, Fantom and Etherlink after April's precautionary LayerZero bridging pause

Partner spotlight:

- YieldBasis V3 markets went live with a reworked HybridVault architecture, and locked YB passed 100M tokens

Llamalend V2: Isolated Lending Markets

Announced on 10 June, Llamalend V2 extends Curve lending from a crvUSD-only system into a framework of isolated lending markets. The core changes:

- With DAO approval, any supported asset can sit on either side of a market; crvUSD is no longer mandatory

- Range-based LLAMMA liquidation protection is now available for all assets pending DAO vote

- Curve LP tokens, yield-bearing vault tokens and principal tokens can now be used as collateral

- Markets now carry an admin fee that flows to Curve DAO. For future crvUSD markets, part of the borrower cost may also be shared with asset issuers or curators, creating an additional incentive to build on crvUSD

- Each market is fully isolated, with borrow caps starting at zero and raised in step with risk review work, subject to DAO approval

The launch is phased, beginning on Optimism before expanding to Ethereum mainnet. The first three markets (ETH/wstETH, wstETH/USDC and WBTC/USDC) were activated through governance in mid-June, backed by a 100K OP incentive campaign distributed via Merkl.

The incentives had an immediate effect: with the OP campaign flowing through Merkl, early borrow rates on the new markets briefly turned negative: at one point borrowers were effectively paid over 50% APR to borrow against WBTC, with the wstETH/USDC market close behind.

LlamaLend V2 is live on @Optimism.

— Curve Finance (@CurveFinance) June 18, 2026

New markets are open, with OP rewards for eligible positions distributed by @merkl_xyz.

Borrow, lend, or loop through isolated markets powered by Curve’s LLAMMA.

Only on Curve — the home of stablecoins.https://t.co/u5HvGpCzsS pic.twitter.com/EItbI3clfX

crvUSD: Peg Holds Through Market Stress

Both months brought a sustained market decline, and crvUSD's stabilisation layers were put to a real test. The peg passed it cleanly, trading between $0.9974 and $1.0001 across the entire period, with no depeg episode at any point.

- PegKeepers retired excess crvUSD from pools as leveraged positions unwound, helping keep the peg stable throughout the decline.

- Borrowers de-risked into falling BTC and ETH, and the system absorbed the deleveraging smoothly, with soft-liquidations and peg defences working in tandem

- The share of crvUSD held in scrvUSD climbed from ~36% to ~66%, with demand for the savings rate holding up even as minting shrank

The contraction in borrowing reflected healthy deleveraging rather than stress on the peg. LLAMMA soft liquidations, PegKeepers and new YieldBasis V3 demand all helped keep crvUSD stable.

Building Recovery in Public

On 1 May, Curve opened a market-based recovery for lenders left with impaired claims in the CRV-long Llamalend market after the October 2025 crash. A dedicated crvUSD/cvcrvUSD pool lets affected lenders swap vault claims for liquid crvUSD at market pricing rather than only waiting, with three voluntary paths: exit, hold, or provide liquidity. Solvency was modelled against the CRV price: claims are modelled to begin recovering around ~$0.957, with full recovery modelled near ~$1.242, framed as gradual rather than guaranteed. Uptake was swift: within the first week the recovery pool drew $141k in liquidity, with over 3% of all vault tokens deposited.

Separately, borrowers of the sDOLA-long2 market (impaired by a March exploit affecting 27 positions) were addressed through a dedicated veFunder fundraising gauge of up to 5M CRV (Vote 1437).

Partner Spotlight: YieldBasis V3

YieldBasis, a protocol building BTC and ETH liquidity on top of Curve infrastructure, rolled out its V3 architecture during May and June, becoming one of the first protocols to deploy Curve’s upgraded FXSwap implementation in production. Approved through governance (Vote 1408), the new implementation reduces value lost to arbitrage during pool rebalances, improving LP returns and fee capture. Because these improvements are built into Curve itself, every future protocol building on FXSwap benefits from the same execution gains without requiring protocol-specific changes.

YieldBasis V3 demonstrates how these primitives can be composed into higher-level products. Its upgraded HybridVaults pair the new FXSwap pools with a dedicated crvUSD allocation alongside crypto assets. Beyond reducing impermanent loss, the HybridVaults create persistent demand for crvUSD, acting as a long-term supply sink. Together with growing scrvUSD adoption, they represent another productive destination for crvUSD beyond borrowing alone. As more applications create sustained demand in this way, newly minted crvUSD is more readily absorbed by productive use cases rather than immediately returning to the market, supporting peg stability and helping maintain attractive borrowing conditions for future issuance.

YieldBasis also optimized its HybridVault architecture by reducing the vault’s crvUSD allocation from 55% to 45%, completed post-audit improvements to its lending oracle with new EMA-smoothed pricing and pool-pressure components, and expanded its analytics dashboard with live market PPS, LP returns, veYB revenue, gauge emissions and protocol fee tracking.

By the end of June, more than 100 million YB had been locked. During the month’s elevated volatility, the upgraded FXSwap pools processed increased trading activity while YieldBasis continued to create structural demand for Curve liquidity and crvUSD. YieldBasis V3 demonstrates how protocols can build differentiated products on top of Curve’s primitives while reinforcing the broader ecosystem through additional trading volume, fee generation and sustained demand for crvUSD.

These @yieldbasis users seemingly earn 20-30% APR on ETH (thanks to volatility) while earning 5% on USD (thanks to @CurveFinance) at the same time https://t.co/wpEjLJ7CNG pic.twitter.com/zCX0XaQL0F

— Michael Egorov (@newmichwill) June 9, 2026

Llamalend V1 Deprecation

Ahead of V2, LlamaRisk coordinated a sweep to deprecate idle and legacy Llamalend V1 markets across four chains. A series of votes raised loan discounts to 50%, swapped monetary policies to flatter curves, and killed unused gauges on Optimism (Vote 1409), Fraxtal (Vote 1410), Arbitrum (Vote 1414) and Ethereum (Votes 1416 and 1422).

Active markets were left untouched, while inactive markets were gradually wound down ahead of the broader migration to Llamalend V2.

Security: vsdCRV Incident Response

On 27 May, StakeDAO's vsdCRV token suffered an exploit. No Curve contracts were affected, but the incident touched the crvUSD/asdCRV Llamalend market on Arbitrum, where asdCRV serves as collateral.

The response was same-day: Curve publicly advised borrowers to repay and exit the market, prompting a controlled exit with the largest single repayment at $417k, and governance killed CRV emissions for the related pool and market (Vote 1418). StakeDAO has since opened a compensation programme for affected holders.

Pool Parameters and Incentives

TricryptoUSDT (USDT/WBTC/WETH) was re-parameterised (Vote 1412), ramping its A parameter and committing new fees. According to Curve’s weekly reporting, the pool generated roughly three times the fees of TricryptoUSDC during its first three days. FXSwap also received an upgraded pool implementation (Vote 1408), reducing value lost to arbitrage during rebalances; YieldBasis pools are among the first to benefit. The alETH pools likewise underwent A parameter ramps. Optimisations like these improve LP and veCRV returns while preserving a competitive execution.

Around twenty new gauges were added across May and June, spanning frxUSD pairs, Tangent Finance’s USG (a stablecoin designed around crvUSD), Vetro’s VUSD suite—which also launched on StakeDAO in partnership with Curve—and pools from 3Jane, Avant and others. A Curve Strategic BTC Reserves pool and a new MIM-2pool gauge rounded out the additions. Fidelity’s tokenised money market fund, $FIDD, also began trading in Curve pools.

VUSD / crvUSD and crvUSD / sVUSD are live on @StakeDAOHQ.

— Vetro (@vetro_org) June 25, 2026

Provide liquidity and earn rewards, in partnership with @CurveFinance.

Links below. pic.twitter.com/7ZMxIjMysu

Cross-Chain and Treasury

CRV bridging resumed across all previously paused networks. Curve had paused its LayerZero bridge infrastructure in April as a precaution after the rsETH LayerZero exploit, and with the review complete the DAO re-enabled bridges on Sonic and Avalanche (Vote 1402), then Fantom and Etherlink, with conservative 10K CRV limits per chain (Vote 1439). The Fantom unpause was timely: the Fantom Opera network was retired on 30 June, and Curve urged remaining LPs to withdraw ahead of the shutdown.

On the treasury side, a proposal to redirect Arbitrum and Base L2 fees to the DAO's treasury passed, alongside routine emissions cleanup on deprecated pools.

Curve at Stable Summit: NYC

On 4 June, Curve hosted Stable Summit IV: NYC, gathering the stablecoin builders shaping DeFi market structure, a follow-up to the Cannes edition covered in the March recap. The event reinforced Curve’s role as infrastructure for stablecoins, productive liquidity and protected borrowing.

A mistake many stablecoin issuers can run into after launch.

— Stable Summit 🦫 (@stable_summit) June 25, 2026

Maximilian Roszko ( @MaxRoszko ) from @CurveFinance on why product market fit is the metric worth optimising for first: pic.twitter.com/2WR51YNWhv

LlamaRisk Concludes Its Curve Engagement

LlamaRisk announced it would conclude its Curve engagement, effective 30 June, as it takes up an expanded mandate as Aave's sole external risk provider. After years of risk work across crvUSD, Llamalend and pool listings, the team departs with the DAO's thanks and returned the unvested remainder of its crvUSD stream to the treasury (Vote 1441).

veCRV: Fees and Revenues

For CRV lockers, volatility translated into revenue. DEX fees came to ~$1.87M in May and ~$2.68M in June; weekly fees peaked near $491k in May and $1.21M during the sharpest selloff week in early June. veCRV APR climbed to ~5.4%, with weekly distributions to veCRV averaging ~$114k in May and ~$138k in June.

Looking ahead, Michael Egorov signalled more crvUSD-friendly veCRV votes on the way.

Some crvUSD-friendly veCRV votes incoming, I am hearing https://t.co/zHIsp9m6IK

— Michael Egorov (@newmichwill) June 27, 2026

Conclusion

Across May and June, borrowers briefly enjoyed negative borrow rates on Llamalend V2, veCRV APR climbed to around 5.4% on record fee generation, new pools and gauges expanded the ecosystem, and crvUSD maintained its peg throughout the market downturn.

As Llamalend V2 expands from Optimism to Ethereum mainnet, isolated lending markets, broader collateral support and new DAO revenue streams position Curve for its next phase of growth as core liquidity infrastructure for stablecoins.