Building recovery in public and building stronger systems next

Affected by the CRV-long LlamaLend market? A new approach could offer more flexibility — giving users the option to exit, hold, or engage in recovery through a transparent onchain market.

The October 10, 2025 market crash put large parts of DeFi under stress. A number of lending protocols were affected. On Curve, some permissionless Llamalend markets using volatile collateral accrued bad debt after sharp price moves and rapidly changing liquidity conditions.

One of those markets was the CRV-long Llamalend market. Since then, some lenders have faced impaired withdrawals and prolonged uncertainty around their deposited funds.

That has left affected users in a difficult position, and it is clear that market solvency and bad debt risk needed to be surfaced more clearly.

At the same time, these positions remain onchain, transparent, and open to market-based resolution. A new path is now being implemented that uses Curve’s own infrastructure to create liquidity around these claims and give affected users an additional voluntary option.

A Market-Based Recovery Path

The practical question is what affected lenders can do with those claims today.

Rather than waiting on a single eventual outcome, this path uses existing Curve primitives to create a dedicated pool between:

- crvUSD, Curve’s decentralized stablecoin

- cvcrvUSD, the vault share token representing lender claims on the affected CRV-long market

In practical terms, a pool structure like this allows affected lenders to swap vault claims for liquid crvUSD at market pricing, rather than only waiting for recovery over time.

That creates multiple voluntary paths for users:

- exit by selling claims into available liquidity

- hold claims if they believe recovery improves over time

- provide liquidity and earn fees, and potentially CRV incentives, for users who understand the risks

This does not remove losses or guarantee recovery. It creates a market where claims can trade, liquidity can form, and users can choose between exiting, holding, or providing liquidity based on their own risk tolerance and time horizon. If market conditions improve, those claims may recover further in value over time, and this pool structure gives the market a way to price those views onchain.

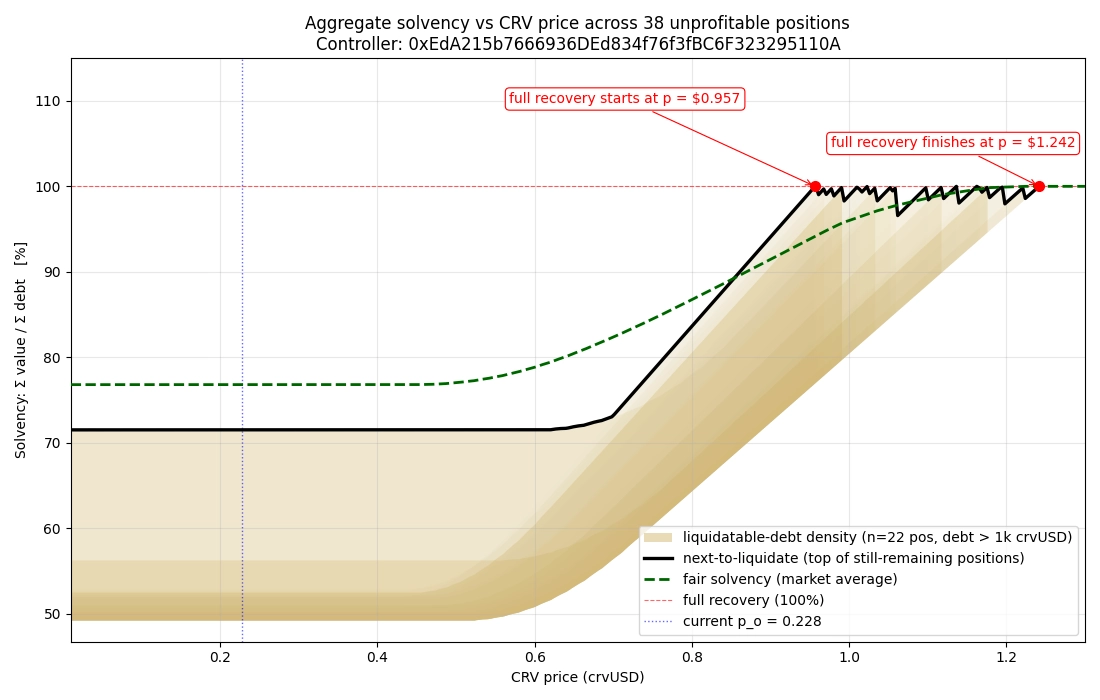

How Market Solvency Changes With CRV Price

The chart below shows how aggregate solvency across the remaining unprofitable positions in the affected CRV-long market changes as the CRV price rises.

At the current reference price, shown by the dotted blue vertical line, those positions remain below full recovery. As the CRV price increases, aggregate solvency improves and a larger share of the remaining shortfall becomes covered.

Two modelled levels are especially relevant:

- Around $0.957 CRV* — recovery starts, with some impaired debt becoming fully covered

- Around $1.242 CRV* — modelled full recovery, where the remaining impaired positions become fully solvent

The key point is that recovery is not binary. It can improve gradually as collateral conditions improve, which is why claims on the affected vault may still have market value today.

*These levels are model-based scenarios, not guarantees.

How Incentives Could Support Recovery

This pool can function on its own, but a gauge could make it more effective.

If a gauge is added, veCRV voters would be able to direct CRV emissions toward the pool. Those incentives could help:

- deepen crvUSD-side liquidity

- improve exit conditions for affected lenders

- attract arbitrageurs and market makers

- support more efficient market pricing

In practice, that would help make the recovery market deeper and more usable, but it is not required for the pool structure itself to exist.

What Has Changed

Market health in Llamalend has always been visible onchain, and community tools such as CurveMonitor and crvHub have long helped users track solvency, utilization, positions, and market conditions.

What has improved since is the visibility of that information in the interface and in supporting documentation.

Curve has since added clearer indicators around market solvency and bad debt, making already-public market information easier to interpret. Documentation is also being expanded around bad debt, market solvency, and lending market risk, so users have clearer context when evaluating these systems.

In some cases, the interface may also limit or discourage interaction with affected markets while those risks remain elevated.

What This Means for Llamalend V2

Llamalend V1 showed that fully permissionless lending markets are possible. It also made clear that volatile collateral markets need stronger market standards, clearer risk signaling, and better parameterization than V1 provided.

Those lessons are directly informing Llamalend V2.

Llamalend V2 is being developed with stronger focus on:

- clearer market standards

- tighter parameterization

- clearer user-facing risk signals

- stronger alignment between market design and incentives

- a more robust lending architecture overall

Llamalend V2 is intended to improve market standards, review, and risk signaling for future markets, not to eliminate risk altogether.

The goal is to make future markets more resilient and reduce the likelihood of similar outcomes.

Looking Ahead

The CRV-long market issue has been frustrating for affected users.

The recovery path now being implemented creates a new voluntary option, but it is not a guaranteed outcome. Recovery may take time and remains dependent on liquidity, market conditions, and any additional governance actions that may follow.

Appendix: Governance Discussions and Proposals

For users who want to explore the full context, technical discussions, and alternative approaches considered by the community, the following governance threads provide additional detail:

- CRV-long LlamaLend Market: Next Steps

- CRV-long LlamaLend Market Recovery Proposal

- Temp Check: Use Treasury Funds to Repay Bad Debt

- Proposal to Compensate for the wFRAX Markets Bad Debt

These discussions reflect the range of perspectives considered — from treasury-backed solutions to market-based recovery mechanisms — and highlight the open governance process behind the current approach.