Introducing Llamalend v2

Open lending markets, LP collateral, isolated risk, and a deeper connection between Curve’s DEX and lending infrastructure.

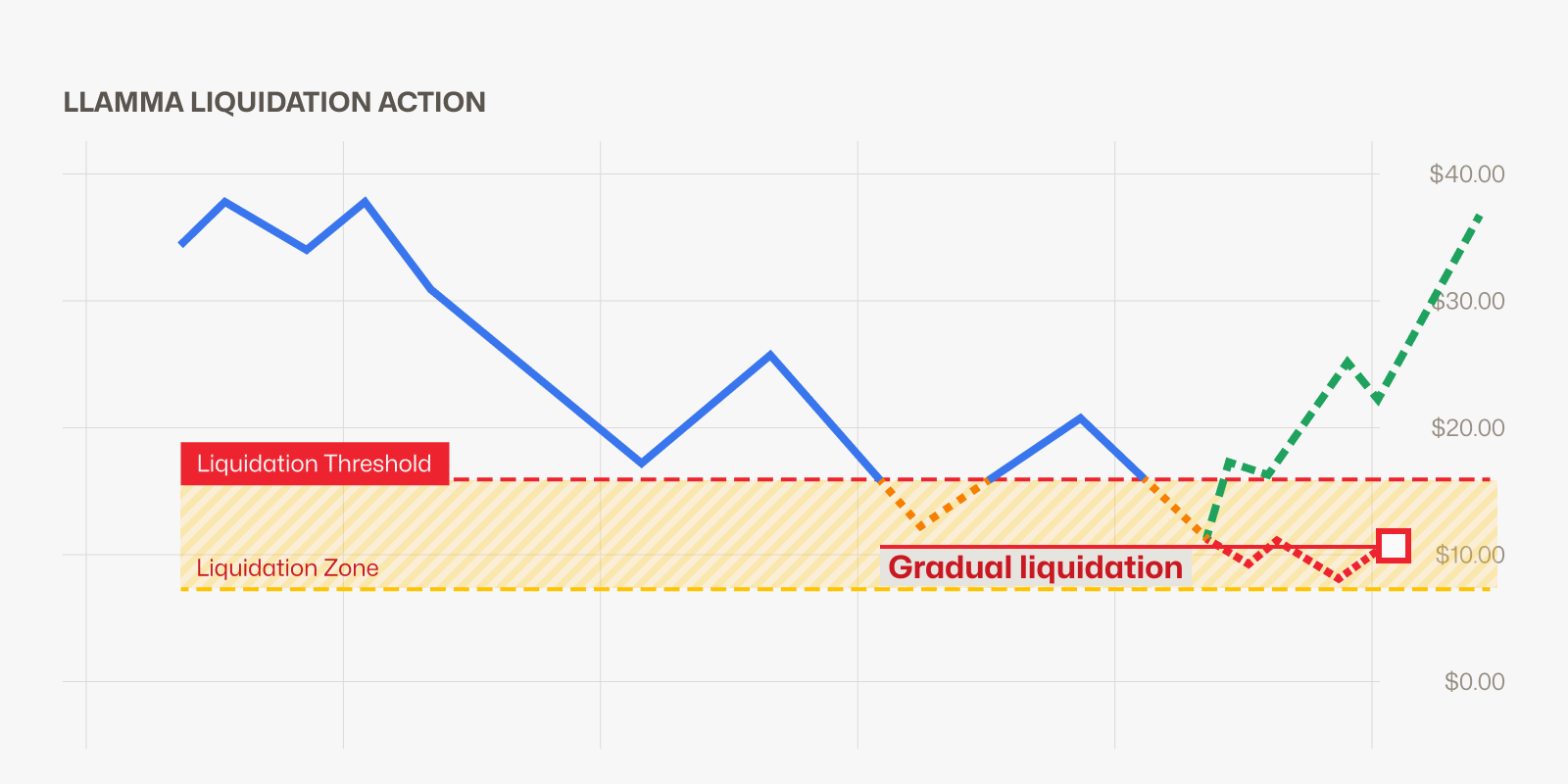

In early 2024, Curve launched Llamalend, a non-custodial lending infrastructure powering Curve’s decentralized stablecoin crvUSD. One central idea behind its design was to replace fixed-price liquidation mechanics with a range-based liquidation system.

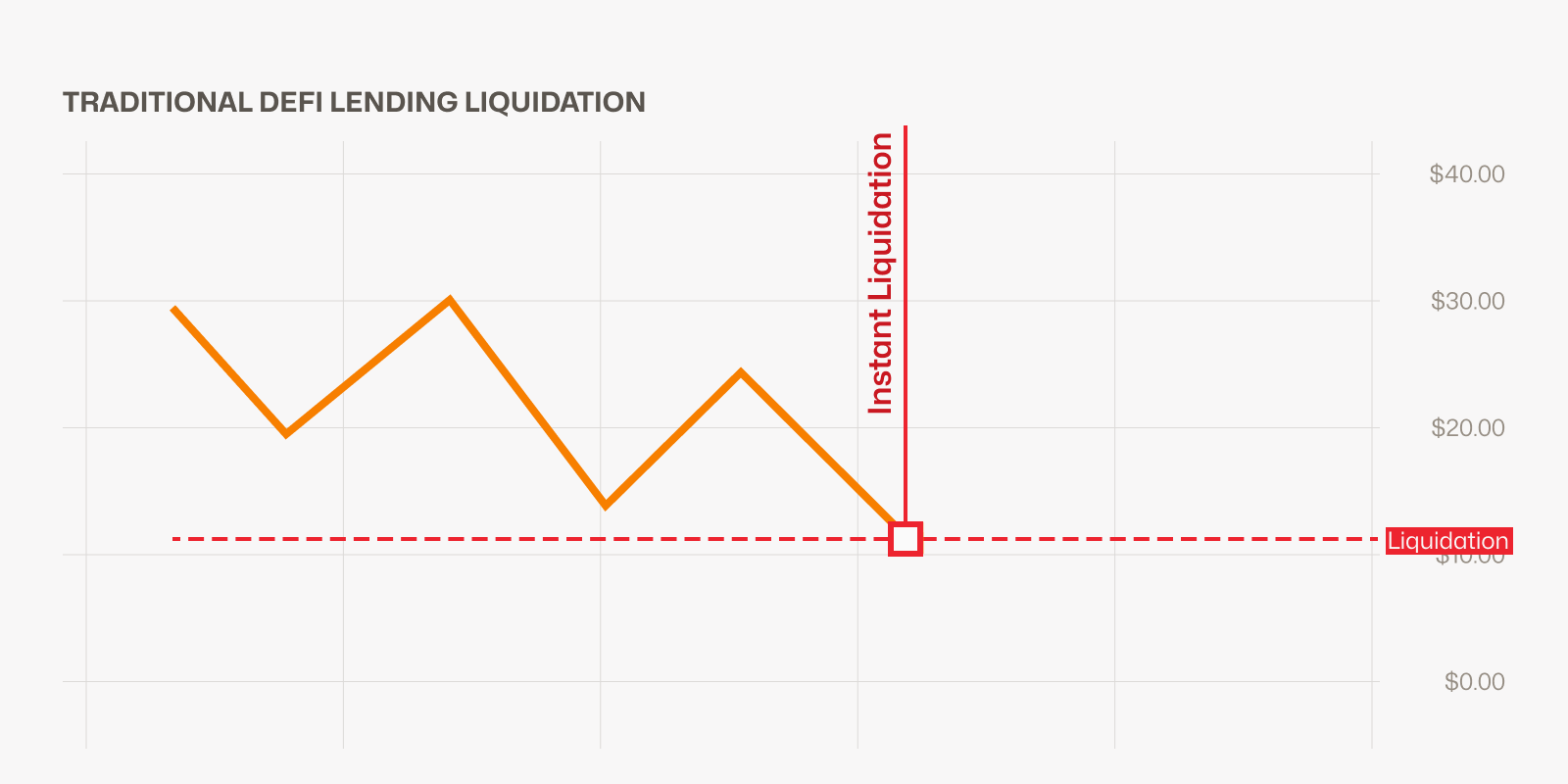

Most DeFi lending protocols liquidate at a single threshold. When collateral value falls to that point, the position is closed, and the collateral is sold. If many positions share similar thresholds, this concentrates selling pressure during the same market move. Prices fall, more positions become unsafe, and liquidation pressure feeds into itself.

That is what Llamalend was designed to address.

The key change is that liquidation is not treated as one event occurring at one price. Each position has a liquidation range. When collateral value enters that range, the system gradually converts collateral into the borrowed asset, rather than closing the position all at once. This gives borrowers more time to react during fast-moving markets and reduces the risk of instant, cliff-edge liquidations. DeFi power users can even benefit from close to full recovery on bounces.

Recent market stress has reinforced why this matters. Lending markets are tested when prices move quickly, liquidity thins, and liquidations become harder to manage. Llamalend v2 builds from that reality. It extends the protocol beyond crvUSD borrowing into a broader system of isolated lending markets, with more supported assets, more collateral types, and a closer connection to Curve liquidity. Under isolation, each market carries its own risk parameters, keeping exposure contained and giving both users and asset issuers a more precisely configured lending environment.

Llamalend v2 turns Llamalend from a crvUSD-focused lending system into a broader framework for Curve markets.

From crvUSD-only to Open Lending Markets

Llamalend v1 was built around crvUSD as the borrowed asset. That made it useful for crvUSD-native lending and bootstrapping crvUSD liquidity, but limited Llamalend’s reach. Asset issuers with their own tokens, protocols building around non-crvUSD pairs, borrowers who needed other assets did not have a straight path through Llamalend.

Llamalend v2 removes that restriction. Range-based liquidation protection is now available for all supported assets by default. With the DAO's approval, markets can now be created with supported assets on both sides: one as collateral, the other as the borrowed asset, without making crvUSD mandatory.

For asset issuers, this creates a clearer path from liquidity to lending. An issuer can build trading liquidity on Curve, then create a lending market around the same asset. This enables them to have both primary and secondary markets in one venue and benefit from Curve's trusted infrastructure for all Users who hold the asset can borrow against it, making the asset more useful, supporting borrowing demand, and helping liquidity become more durable. The DEX and the lending market become parts of the same usage loop.

For the Curve DAO, the removal of the crvUSD requirement also changes the economics. Non-crvUSD markets will be able to carry an admin fee that flows to the Curve DAO, giving Llamalend a clearer role in Curve's long-term economics.

Lending Built on Top of Liquidity

The second major change expected with Llamalend v2 is the use of LP tokens as collateral.

In many DeFi systems, providing liquidity and borrowing against capital are separate decisions. The same capital usually cannot do both at once.

Llamalend v2 changes that.

Curve LP tokens can now be used as collateral in lending markets. A user can provide liquidity to a Curve pool, keep exposure to trading fees, and borrow against that position at the same time.

This makes lending more closely connected to Curve’s liquidity layer. Liquidity does both support trading and borrowing capacity, giving LP positions another use inside the Curve ecosystem, and strengthening the revenue flows across the product suite.

The same idea can extend to other productive collateral types, including yield-bearing vault tokens and principal tokens used in fixed-yield strategies. A position that earns yield on its own can also back a loan, which means capital is no longer locked into one role.

Curve DEX and its LLAMMA powered lending markets become parts of the same loop

Risk Managed Market by Market

More flexible markets need stronger risk boundaries. A stablecoin market, an ETH market, an LP-token market, and a fixed-yield asset market all behave differently. They should not be managed with the same assumptions.

Llamalend v2 keeps markets isolated, with each market having its own collateral asset, borrowed asset, parameters, caps, oracle setup, and risk profile. Borrow caps start at zero, and markets need DAO approval before debt can be built. For the initial rollout, LlamaRisk is reviewing proposed markets for Llamalend before they move through governance.

For asset issuers, this creates a useful benchmark. A lending market depends on more than the asset itself. It needs reliable liquidity, a credible oracle design, and parameters that match how the market actually behaves.

Curve can support issuers first on the DEX side, helping build the liquidity base needed before a lending market is ready to move through governance. If an asset can cross that line, it is a strong signal that its onchain market has reached a higher level of maturity.

Launching Llamalend v2

Llamalend v2 will launch in phases, starting on Optimism before expanding to Ethereum mainnet.

The initial deployment will include three isolated lending markets:

As per the new safety measures, these markets will initially launch with borrow caps set to zero. This allows to validate deployment parameters, observe market behavior, validate integrations, and ensure the system operates as expected before borrowing is enabled.

To support the launch, an incentive campaign powered by Merkl will distribute 100,000 OP tokens across the initial markets.

Borrowing will be enabled once the Curve DAO approves the first borrow cap increases through governance. As with all Curve DAO votes, this process takes approximately seven days from proposal to execution.

Launching with zero borrow caps reflects the same market-by-market risk approach that underpins Llamalend v2. Markets are deployed first, observed in production, and then progressively opened as governance gains confidence in their operation.

Following a successful rollout on Optimism, additional Llamalend v2 markets will be deployed on Ethereum mainnet.

Asset issuers interested in launching lending markets on Llamalend v2 are encouraged to reach out to the Curve team. As discussed earlier, a successful lending market depends on more than the asset itself: liquidity, oracle design, and risk parameters all play a critical role in creating a healthy market.

Users who encounter issues, unexpected behavior, or have feedback on the new system are also encouraged to get in touch as Curve continues to iterate on the next generation of its lending infrastructure.

What v2 Prepares Curve for

Llamalend v2 turns Llamalend from a crvUSD-focused lending system into a broader framework for Curve markets.

The important change is that lending can now sit closer to the liquidity Curve already helps create. An asset can build depth on the DEX, become more useful as collateral, and eventually support a lending market around the same onchain liquidity base.

That matters for users because capital can move across more roles inside Curve. Just as important it is for asset issuers, because a Curve pool can become the starting point for a deeper market structure. And it eventually matters for the DAO, because lending activity can become a larger part of Curve’s long-term economics.

V2 keeps the original idea behind Llamalend: liquidation should be handled through a range, instead of through a single cliff-edge event alone. What changes is the scope: that design can now support a wider set of markets, with risk handled market by market as the system grows.